Lifetime Health Cover Loading: It Gets More Expensive the Longer You Put It Off

Lifetime Health Cover (LHC) loading. Four words costing Australian’s thousands of dollars in their thirties, forties and beyond. What’s worse, is this whole thing is avoidable. If only someone cared to explain this government rule to us in a human-way earlier. Hello, friends. We’re that special someone and we’re here to tell you why you need to start caring about LHC loading before it takes care of you.

But, first a poll!

Are you under 30?

This article is your hack to avoid LHC loading, period. Saving you hundreds to thousands of dollars in the long run.

Are you over 30, and don’t currently have private hospital cover?

Read this article and end the loading now! We’re so glad you found this, let’s break it down for you.

What Is Lifetime Health Cover (LHC) Loading?

Basically, LHC loading is like a financial slap on the wrist for not getting private hospital cover before July 1st, after you turn 31. It’s applied automatically at tax time. They have your date of birth and aren’t afraid to use it. And for every year you don’t have cover, your future premiums will go up by 2%. So no matter how good a deal you find, it all adds up real quick.

The worst part? It’s cumulative and can reach up to 70%. Yep, you read that right. Imagine finally signing up for private hospital cover (because you likely need it), only to have to shell out an extra 70% of LHC loading? Nightmare.

But LHC loading doesn’t stick around forever. This pesky percentage disappears after 10 years of continuous coverage. See ya, pesky fees.

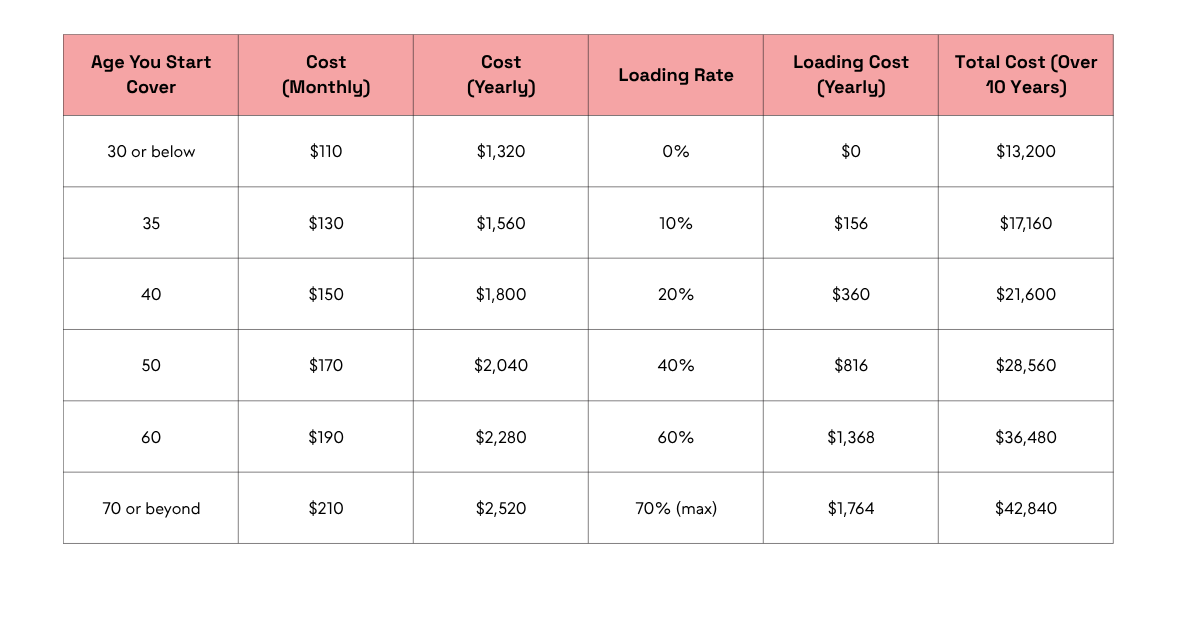

What LHC could cost you

Here’s an example of how LHC loading can really creep up on you the longer you're uninsured:

Base Premium: $110 per month

LHC Loading Rate: 2% per year over 31

for illustrative purposes only

This means that if you waited until you were 40 to get private hospital cover, you would be paying an extra 20% every month – or a casual $8,400 more over 10 years, than if you’d just taken out eligible private health insurance when you’d turned 31.

The loading stings more the longer you wait, as you can see with our friends in the 50+ bracket.

Why Should You Care About LHC Loading Now?

I know what you’re thinking, but how much will it actually cost me? I’m 35 and still relatively young and healthy. Can I afford to wait? Hypothetically speaking, could you afford to lose $3,960 that might otherwise have been put towards your investments? Because that’s the difference in loading paid between 30 and 35-year-olds alone. ‘

Here’s what you stand to gain from getting your private health cover sorted, now:

Long-Term Savings: The sooner you get it, the less you’ll pay in the long run. Even basic hospital cover can save you thousands on loading alone.

Peace of Mind: Private hospital coverage means shorter wait times, more choice in hospitals, and access to specialists when you need them. This is particularly important if you’re planning to start a family, where it’s mandatory to hold private hospital cover for 12-months before you’re even eligible to claim any obstetric or birth services.

It’s Temporary: If you’ve copped the loading, don’t stress too much. It drops off after 10 years of cover. You just need to stick with it.

What Should You Do About LHC Loading Now?

If you’re under 31, you’re ahead of the game! Consider this your gentle nudge to look into private hospital cover. You might even want to factor it into your budgeting for the coming years. (We’ve got a spreadsheetfor that). Even a basic policy can lock in your rate (I.e. 0% LHC loading) so you literally never have to pay it!

And, if you’re over 31, you’ve seen how this thing snowballs. Consider getting private hospital cover now to avoid paying exorbitant LHC loading in future; when you might actually need it, and it could sting most.

Where Should You Start Looking For Private Health Insurance?

Canstar is a good place to start. Then of course, there are comparison sites or you can have a chat with a financial advisor to find something that suits your vibe and your budget.

We believe in you!

***Any financial advice is general in nature and hasn't considered your personal circumstances. Seek advice from a licensed financial adviser and read the relevant PDS.